INDUSTRIAL policy via Twitter is a new development in economics but we may all have to get used to it over the next four (or eight) years. Donald Trump’s tweets on the car industry (and his planned cuts to corporate income tax) may or may not have persuaded Ford to keep a plant in Michigan, creating 700 jobs. But the problem with such headline-grabbing is that there are thousands of companies in America, and jobs are being created or destroyed every day; intervening in all these situations is impossible. Even in cars, for example, GM has recently announced 3,300 lay-offs , almost five times greater than the Ford additions.

History suggests that the aim of creating large numbers of manufacturing jobs will be a lost cause.

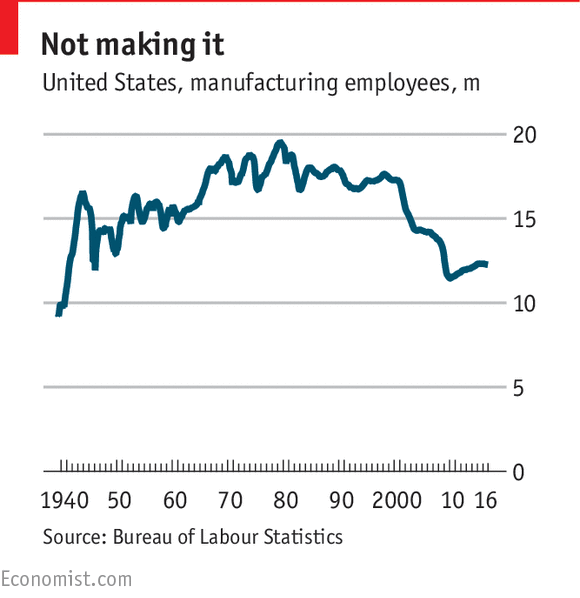

In 1979, the high point for American manufacturing jobs was reached at 19.5m. The subsequent recession of the early 1980s caused that number to fall but there were regularly 17m-18m jobs in the 1980s and 1990s. From the turn of the millennium, however, the total fell pretty remorselessly, with the 2008-09 recession proving the coup de grace. The low was just under 11.5m in early 2010. As the economy recovered, some jobs returned and a peak of 12.3m was reached early last year. But since then, the numbers have been drifting down again

The same kind of declines have been seen across the developed world, indicating that this is not a particular problem of American economic policy. A report from the Congressional Research Service sets the context; America’s share of global manufacturing value added fell 12 percentage points between 1993 and 2014 but Japan’s share fell 14 points over the same period.

Unsurprisingly, China has taken the bulk of the market share.

In terms of employment, the 31% decline in America between 1990 and 2014 compared with a 25% fall in Germany, 33% declines in France and Sweden, 34% in Japan and 49% in the UK.

The problem is not just China but technology.

Industries, like cars and steel, tend to be plagued by overcapacity. There can be good times in the cycle (American car sales are setting new records, for example). The 2008-09 slump caused people to postpone their purchases but eventually confidence recovered; cars wear out and must be replaced. But a downturn will inevitably come;research suggest that consumers’ budgets are stretched, leading them to finance today’s car buys over six to seven years, delaying the next car purchase. A competitive market means that car manufacturers must keep investing to add new features while keeping prices down; that may mean replacing people with machines. It also means that a lot of the value added in a car comes from the software that runs it; jobs that tend to go to college graduates or are not found in rustbelt states. In Britain, the share of low-skilled manufacturing jobs has fallen since the 2008 recession while foreign-born workers comprise 17% of the total, similar to banking. The service sector contributes more than 30% of value added in American manufacturing and more than 40% in France and Italy.

And herein lies the problem of focusing on manufacturing jobs which comprise just 10% of all employment in America (in percentage terms, there has been a virtually uninterrupted . Slapping on tariffs to punish manufacturers who export jobs makes little sense in a world of global value chains, every dollar of Mexican goods exported to America contains 40 cents of American goods embedded within it. Worse still, the disruption to trade in services that might result, let alone the higher prices that consumers would have to pay, would far outweigh the positive impact of keeping a few jobs in America.

The markets seem remarkably sanguine about all this; far more so than they would have done if a President Bernie Sanders were threatening American businesses with retaliation. But we have seen individual stocks take a hit (Boeing , for example) when they came into the Twitter firing line of Mr Trump. Eventually, one thinks, the unpredictability of the attacks will wear out investors’ nerves.

Receive Daily Updates

Recent Posts

Steve Ovett, the famous British middle-distance athlete, won the 800-metres gold medal at the Moscow Olympics of 1980. Just a few days later, he was about to win a 5,000-metres race at London’s Crystal Palace. Known for his burst of acceleration on the home stretch, he had supreme confidence in his ability to out-sprint rivals. With the final 100 metres remaining,

[wptelegram-join-channel link=”https://t.me/s/upsctree” text=”Join @upsctree on Telegram”]Ovett waved to the crowd and raised a hand in triumph. But he had celebrated a bit too early. At the finishing line, Ireland’s John Treacy edged past Ovett. For those few moments, Ovett had lost his sense of reality and ignored the possibility of a negative event.

This analogy works well for the India story and our policy failures , including during the ongoing covid pandemic. While we have never been as well prepared or had significant successes in terms of growth stability as Ovett did in his illustrious running career, we tend to celebrate too early. Indeed, we have done so many times before.

It is as if we’re convinced that India is destined for greater heights, come what may, and so we never run through the finish line. Do we and our policymakers suffer from a collective optimism bias, which, as the Nobel Prize winner Daniel Kahneman once wrote, “may well be the most significant of the cognitive biases”? The optimism bias arises from mistaken beliefs which form expectations that are better than the reality. It makes us underestimate chances of a negative outcome and ignore warnings repeatedly.

The Indian economy had a dream run for five years from 2003-04 to 2007-08, with an average annual growth rate of around 9%. Many believed that India was on its way to clocking consistent double-digit growth and comparisons with China were rife. It was conveniently overlooked that this output expansion had come mainly came from a few sectors: automobiles, telecom and business services.

Indians were made to believe that we could sprint without high-quality education, healthcare, infrastructure or banking sectors, which form the backbone of any stable economy. The plan was to build them as we went along, but then in the euphoria of short-term success, it got lost.

India’s exports of goods grew from $20 billion in 1990-91 to over $310 billion in 2019-20. Looking at these absolute figures it would seem as if India has arrived on the world stage. However, India’s share of global trade has moved up only marginally. Even now, the country accounts for less than 2% of the world’s goods exports.

More importantly, hidden behind this performance was the role played by one sector that should have never made it to India’s list of exports—refined petroleum. The share of refined petroleum exports in India’s goods exports increased from 1.4% in 1996-97 to over 18% in 2011-12.

An import-intensive sector with low labour intensity, exports of refined petroleum zoomed because of the then policy regime of a retail price ceiling on petroleum products in the domestic market. While we have done well in the export of services, our share is still less than 4% of world exports.

India seemed to emerge from the 2008 global financial crisis relatively unscathed. But, a temporary demand push had played a role in the revival—the incomes of many households, both rural and urban, had shot up. Fiscal stimulus to the rural economy and implementation of the Sixth Pay Commission scales had led to the salaries of around 20% of organized-sector employees jumping up. We celebrated, but once again, neither did we resolve the crisis brewing elsewhere in India’s banking sector, nor did we improve our capacity for healthcare or quality education.

Employment saw little economy-wide growth in our boom years. Manufacturing jobs, if anything, shrank. But we continued to celebrate. Youth flocked to low-productivity service-sector jobs, such as those in hotels and restaurants, security and other services. The dependence on such jobs on one hand and high-skilled services on the other was bound to make Indian society more unequal.

And then, there is agriculture, an elephant in the room. If and when farm-sector reforms get implemented, celebrations would once again be premature. The vast majority of India’s farmers have small plots of land, and though these farms are at least as productive as larger ones, net absolute incomes from small plots can only be meagre.

A further rise in farm productivity and consequent increase in supply, if not matched by a demand rise, especially with access to export markets, would result in downward pressure on market prices for farm produce and a further decline in the net incomes of small farmers.

We should learn from what John Treacy did right. He didn’t give up, and pushed for the finish line like it was his only chance at winning. Treacy had years of long-distance practice. The same goes for our economy. A long grind is required to build up its base before we can win and celebrate. And Ovett did not blame anyone for his loss. We play the blame game. Everyone else, right from China and the US to ‘greedy corporates’, seems to be responsible for our failures.

We have lowered absolute poverty levels and had technology-based successes like Aadhaar and digital access to public services. But there are no short cuts to good quality and adequate healthcare and education services. We must remain optimistic but stay firmly away from the optimism bias.

In the end, it is not about how we start, but how we finish. The disastrous second wave of covid and our inability to manage it is a ghastly reminder of this fact.